Lender Resources

Access a wide range of guidelines, informational resources, and sample documents to assist with effectively managing insurance tracking and maintaining flood insurance requirements while ensuring compliance. By leveraging these documents and guidelines, lenders can streamline their processes, reduce administrative burdens, and enhance their interactions with borrowers. These materials are continually updated to reflect the latest regulatory changes, providing a reliable and centralized resource for mortgage servicing best practices.

Private Flood Insurance Acceptance Criteria

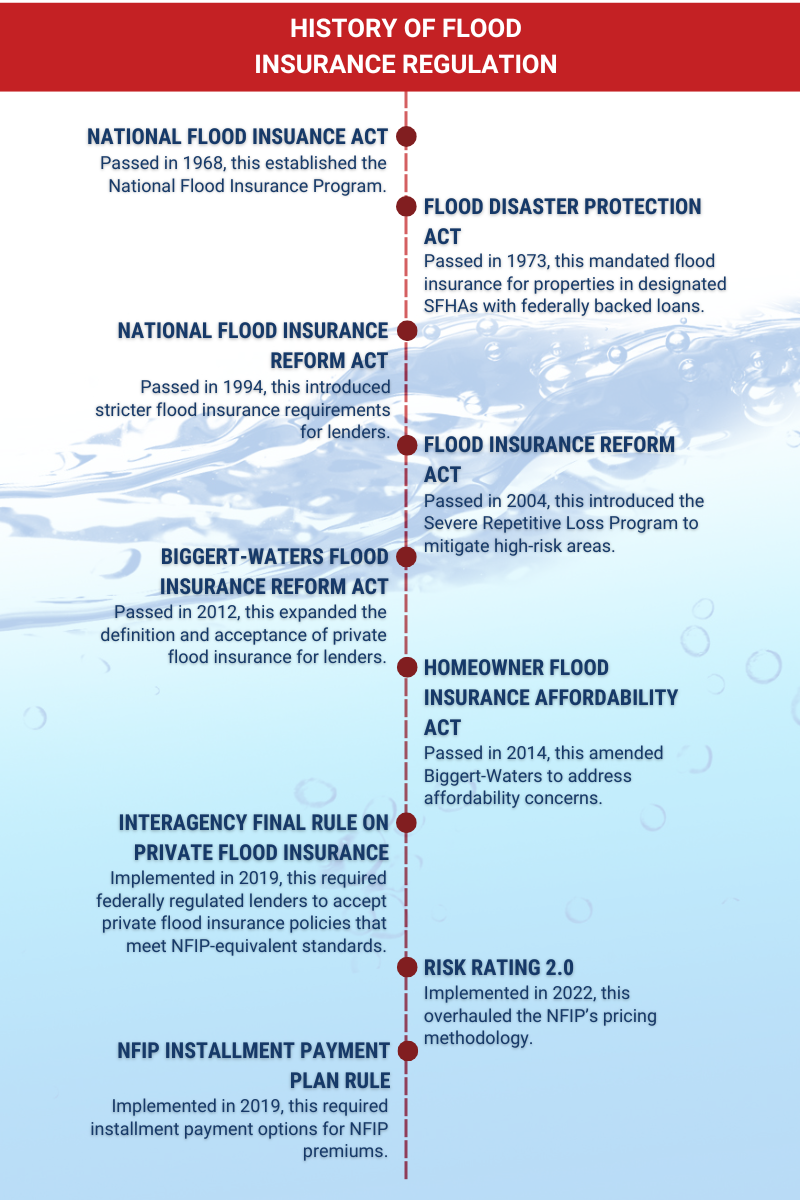

Private flood insurance must meet specific requirements defined under 42 U.S. Code § 4012a, as outlined in the Biggert-Waters Flood Insurance Reform Act of 2012.

If a private policy includes the “Compliance Aid Clause” no further analysis is necessary for the lender to accept the policy. If this clause is not present, lenders must review the proposed policy to ensure it meets all of the following requirements.

Be Issued by an Approved Insurer:

The insurance company must be licensed, admitted, or otherwise approved to operate in the state or jurisdiction where the insured building is located.

Alternatively, for certain policies covering commercial properties (e.g., difference in conditions, multiple peril, or all-risk policies), the insurer must be recognized or not disapproved as a surplus lines insurer in the state or jurisdiction.

Provide Equivalent Coverage:

The policy must offer flood insurance coverage that is at least as broad as the coverage provided by the National Flood Insurance Program (NFIP). This includes comparable deductibles, exclusions, and policy conditions.

Include Key Provisions:

Cancellation/Non-Renewal Notice: Insurers must provide 45 days’ written notice of cancellation or non-renewal to:

- The insured party, and

- The lender (either a regulated lending institution or a federal agency lender).

NFIP Information: The policy must include details about the availability of NFIP flood insurance.

Mortgage Clause: The policy must contain a mortgage interest clause, similar to that in standard NFIP policies.

Legal Action Timeline: The policy must require any legal action (e.g., lawsuits for claim denials) to be filed within 1 year from the date of the written denial.

Restrictive Cancellation Provisions:

Cancellation terms must be as strict as those in NFIP standard flood insurance policies.

This ensures private flood insurance provides borrowers and lenders with protections and coverage equivalent to NFIP policies.

Forms and Sample Notices

Standard Flood Hazard Determination Form (SFDHF)

The SFHDF is a critical tool for managing flood risk in real estate transactions and protecting lenders, borrowers, and properties from the financial impacts of flooding.

Mandated by the National Flood Insurance Act of 1968, this form is used by lenders to determine whether a property is located in a Special Flood Hazard Area (SFHA).

Sample Borrower Notice of Special Flood Hazards

The Borrower Notice of Special Flood Hazards is used when a lender determines that a property securing a loan is located within a Special Flood Hazard Area (SFHA). This notice must be provided when a lender originates, increases, extends, or renews a loan secured by a building or mobile home located within an SFHA. This requirement applies to loans originated, purchased, or serviced by federally regulated financial institutions, as well as loans secured by mortgages backed by federal agencies.

If the property is located in a community that has chosen not to participate in the NFIP or has been suspended from the program for failing to adopt or enforce floodplain management regulations, the borrower must still be notified of the fact their their property is located in a SFHA. While flood insurance may be unavailable through the NFIP due to non-participation, lenders are still required to notify the borrower of the flood risk and explain the implications and they may assist the borrower in identifying private flood insurance options.

Sample Borrower Notice of Non SFHA Location

While not federally required, lenders often issue a notice informing property owners that a structure is not located in a Special Flood Hazard Area (SFHA) to:

- Ensure transparency and build trust with borrowers.

- Confirm flood risk assessment results.

- Document communication in case of disputes or errors.

This is used if a flood zone determination indicates that the property is in a moderate or low-risk flood zone.

Sample Borrower Notice of Option to Escrow

The Option to Escrow Notice helps borrowers understand their rights and options for managing flood insurance payments, while ensuring lenders comply with federal flood insurance regulations. Under the Biggert-Waters Flood Insurance Reform Act of 2012 and subsequent regulations, this notice is required to inform borrowers of their right to escrow flood insurance premiums and fees.

Lenders must provide this notice when a loan secured by a building or mobile home is made, increased, extended, or renewed and:

- The property is located in a SFHA.

- Flood insurance is required as a condition of the loan.

NFIP Community Status Book

The NFIP Community Status Book is an essential tool for understanding a community’s relationship with the NFIP and ensuring compliance with flood insurance and risk management regulations. It is widely used by lenders, insurers, policymakers, and property owners to make informed decisions regarding flood insurance and development in flood-prone areas.

The NFIP Community Status Book is an essential tool for understanding a community’s relationship with the NFIP and ensuring compliance with flood insurance and risk management regulations. It is widely used by lenders, insurers, policymakers, and property owners to make informed decisions regarding flood insurance and development in flood-prone areas.

Maintained by the Federal Emergency Management Agency (FEMA), the NFIP Community Status Book provides detailed information about communities participating in the National Flood Insurance Program (NFIP). It serves as a reference for understanding the status of communities in relation to the NFIP, including whether they are active participants, suspended, or ineligible.

FEMA provides the book as a free online resource on its website. It is organized by state for easy access.